Reverse mortgage vs HELOC is something most homeowners don’t think about—until they actually need money. And when that moment comes, it usually isn’t theoretical. This is practical. Real. Sometimes urgent.

Both let you tap home equity — but they work fundamentally differently.

The difference between options is what makes this decision harder than it looks on paper.

If you live in Rhode Island in Providence, Warwick or Cranston, the value of your home may have gone up over time. With the value of homes near $430,000, many homeowners have built up equity in their homes. However, they often do not plan to use this equity.

But then life happens. Retirement. Medical costs. Home repairs. Or sometimes just wanting a bit more breathing room financially.

That’s when the question becomes real: Should you go with a reverse mortgage or a HELOC? No universal answer exists. But there is a right answer for your situation.

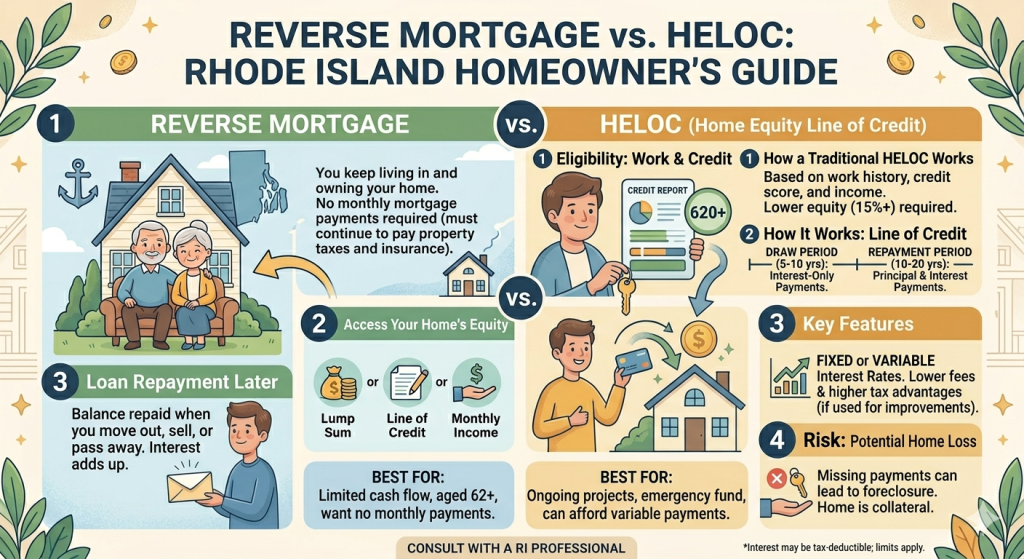

What Is a Reverse Mortgage?

A reverse mortgage is often not understood, mostly because it works in a way that people think it does. If you pay the lender every month, the lender pays you, based on the equity in your home. This is the idea of a reverse mortgage.

Mainly for homeowners age 62 or older. One significant advantage is simple: you don’t make monthly payments.

You still own your home. You continue to live inside it. Nothing changes in that sense. The difference is that the loan balance slowly increases over time instead of decreasing. You repay the loan only later—usually when you sell the home or stop living there.

For many retirees, this setup removes a major source of stress. Not having a monthly payment gives you one less thing to worry about, especially when you have a fixed income.

To understand how they calculate and organize everything, review how reverse mortgage loans work in RI. They explain local criteria rules and payout structures more clearly there.

Another thing worth mentioning is flexibility. A reverse mortgage doesn’t force you into one format. Some people take a lump sum. Others prefer monthly payments. Some keep it as a line of credit for future use.

Many people do not think about the flexibility of mortgages. However, it is very important.

You can also read the complete guide to reverse mortgages, which will explain how these loans function over time.

What Is a HELOC?

A HELOC feels more familiar to most people because it behaves more like traditional borrowing.

A home equity line of credit or home equity line of credit is basically a line of credit that uses your home as security. You do not get all the money at once; you get access to it. Use it when you need it.

That’s what makes it appealing. You borrow a little now, maybe more later, and only pay interest on what you actually use.

At first, it can feel quite manageable. During the initial phase, payments are often low because you’re mostly paying interest. That creates a sense of control. But the second phase changes things.

At some point, you enter the repayment period. That’s when you start paying both principal and interest. And that’s usually when monthly payments go up—sometimes more than expected. People often feel caught off guard here.

HELOCs are better suited for homeowners who have a job and get a steady income. People often use HELOCs for things like renovations, big expenses or term financial needs.

If you’re considering this route, it’s worth taking a closer look at how lenders structure these products locally. You can explore HELOC options in Rhode Island to understand what’s practically available.

Difference Between HELOC and Reverse Mortgage

On the surface, both options seem similar. You’re using your home to access money.

But once you look closer, the difference becomes unmistakably clear—and honestly, it all comes down to one thing:

Monthly payments.

A HELOC requires them. A reverse mortgage doesn’t. That single difference affects everything else.

With a HELOC, you’re actively managing debt. You have to plan for payments, think about interest rates, and stay consistent.

With a reverse mortgage, the pressure shifts. The loan has no monthly obligation, but it grows over time instead. Not just a financial difference—it’s a lifestyle difference.

Side-by-Side Comparison

| Feature | Reverse Mortgage | HELOC |

| Monthly Payments | Not required | Required |

| Age Requirement | 62+ | No restriction |

| Credit Check | Minimal | Required |

| How Funds Are Received | Lump sum, monthly, or line | Flexible credit line |

| Repayment | When home is sold or vacated | Monthly payments |

| Effect on Ownership | You retain ownership | You retain ownership |

When HELOC Makes More Sense

A HELOC is clearly the choice in some cases. This usually depends on when you need the money and how much you earn.

If you have a job and get an income and you can make your monthly payments, a HELOC gives you more freedom. A reverse mortgage does not give you this freedom.

It is also an idea if you do not plan to live in your home for a long time. You might be moving to a house in a few years or might be using the money for a thing you want to do.

In these situations, having a plan to pay back the money is not a problem. You need to think about what might happen in the future. Your income might change & the interest rates might go up.

What you can handle now might be too much for you later. A HELOC is an option when you think about these things.

When HELOC Wins (Younger, Planning to Move, Want Flexibility)

In some situations, a HELOC isn’t just a good option—it’s clearly the better one.

If you’re still in your earning years and your income remains steady, handling monthly payments typically isn’t a challenge. In that case, the flexibility a HELOC provides becomes valuable. You don’t have to follow a fixed structure, and you can use funds only when you actually need them.

It also makes more sense if you don’t plan to stay in your home forever. For example, if you expect to sell in a few years, taking a reverse mortgage may not align well with your timeline. A HELOC, on the other hand, fits short- to medium-term financial planning much better.

Control is another advantage. You decide when and how much to borrow. This flexibility is useful for renovations at home, business investments, and to bridge short-term cash flow gaps.

If you’re comparing borrowing options in detail, read this reverse mortgage vs. HELOC comparison. This video shows the flexibility of real-life situations.

When a Reverse Mortgage Is the Better Fit

A reverse mortgage is something that makes sense when you are at a different point in your life.

If you are 62 or older, and you are living on a fixed income and you plan to stay in your home for a time, then your priorities are going to be different. At this point in your life, having stability is more important to you than having flexibility.

Not having a monthly payment can make a significant difference. It removes pressure and creates predictability.

That’s why many retirees lean toward this option. Maintaining comfort—not maximizing equity—is what it’s about.

Rhode Island Context: Why This Matters More Than You Think

Rhode Island offers a unique experience for homeowners. Property values have been steadily increasing in cities like Providence, Warwick and Cranston. Many homeowners have built equity without trying.

In the same time period, both income and living costs, particularly in retirement, increased. The gap between the two is what causes people to consider reverse mortgages and HELOCs.

Another factor is how lenders evaluate borrowers.

Reverse mortgages focus more on your home and age. HELOCs focus more on your income and credit. That difference alone can change what’s available to you.

How Local Property Trends Affect Your Decision

In Rhode Island, property value trends are more important than many people think. Home values in cities such as Providence, Warwick, and Cranston have steadily increased over the last decade.

Homeowners who purchased their homes years ago have a lot of equity that can be used. It is still true, even if the person’s income of the person hasn’t changed very much.

This is exactly why reverse mortgages are becoming more common among retirees. They allow homeowners to convert that built-up value into cash without selling the property.

At the same time, lenders in Rhode Island review HELOC applications more strictly. They focus on income and credit scores. This makes it harder for retirees to qualify, even if they have substantial equity.

For a full breakdown of state-specific eligibility and payout structures, this resource helps: How reverse mortgage loans work in RI

Long-Term Impact You Should Think About

Most people focus on what happens now. Fewer think about what happens ten years later.

With a HELOC, your payments determine the risk. If interest rates go up, payments can increase. If income changes, those payments can become difficult to manage.

With a reverse mortgage, the trade-off is different. No repayments are needed, but the loan balance grows.

This slowly reduces your equity over time. Neither option is perfect. They just solve different problems.

For a deeper breakdown of these trade-offs, read this in-depth reverse mortgage vs HELOC comparison. It explains the long-term effects in more detail.

The Psychological Side of Debt Most People Ignore

Most comparisons focus on numbers—interest rates, payments, and equity. But there’s another layer that matters just as much: how the loan feels over time.

With a HELOC, you always have an active obligation. Even if payments are manageable, there’s a mental weight that comes with knowing you have to pay every month. That pressure doesn’t affect everyone the same way, but for some homeowners, it becomes stressful over time.

A reverse mortgage creates a different experience. Not having a monthly bill to worry about removes that ongoing pressure. Especially for retirees, it can create a sense of safety and peace that goes beyond just money.

This doesn’t make one option better than the other. It just shows that money decisions aren’t purely mathematical. They are also emotional.

Reverse Mortgage vs Refinancing

Sometimes, people consider refinancing instead of either option.

Refinancing can lower your rate or change your loan structure. It does not remove payments or offer the same flexibility.

If you are comparing all options, it helps to review reverse mortgages vs refinancing. This shows how each fits your financial plan.

What Most Homeowners Regret Later?

Looking back, most homeowners don’t regret choosing a HELOC or a reverse mortgage. They regret not fully understanding what they signed up for.

A common issue with HELOCs is underestimating how payments change over time. What starts as a low, interest-only payment can turn into a much higher monthly obligation later. If you don’t plan for that change, it can create financial strain.

With reverse mortgages, the regret usually comes from not thinking long-term. Because there aren’t any monthly payments, it’s simple to miss how the loan balance increases over time and gradually cuts into equity.

Before making a decision, it’s worth reviewing all angles. To compare this with another option, look at reverse mortgage vs refinancing. It can help you see the differences clearly.

Final Thoughts

No simple answer exists to reverse mortgage vs HELOC. It depends on where you are in life, how stable your income is, and what kind of financial pressure you’re willing to handle.

Some people prefer flexibility. Others prefer stability. Neither is wrong. But choosing the wrong one for your situation can create problems later.

If you’re still unsure, it helps to talk it through with someone who understands the local market.

You can speak with an RI reverse mortgage broker or request a free no-obligation consultation to get clarity based on your situation.

Sometimes, a short conversation is all it takes to make the right decision.