Reverse mortgages enable homeowners aged 62 or over to receive some money. They do not make monthly payments. Instead of paying the lender, the lender pays you.

The person who owns the home pays back the loan when they sell the house. They must repay the loan when they leave the property. They can stay in the property while they handle responsibilities like paying taxes, maintaining insurance, and making repairs.

That’s the idea. If you’re really thinking about getting a reverse mortgage, you need to know more. You need to know how it works over a time.

This issue comes up more often than most people realize in Rhode Island. Home values in cities like Providence, Warwick, and Cranston have steadily increased, reaching an average of around $430,000. Many homeowners are equity-rich without planning to be. The house they bought years ago has quietly become their largest financial asset.

The challenge is not whether that value exists. The challenge is how—and when—to use it without creating problems later.

What Is a Reverse Mortgage?

A reverse mortgage is not only a “loan without payments.” While technically correct, this definition ignores the logic behind it.

The most common type of this product is known as a Home Equity Conversion Mortgage (HECM). The federal government ensures it. It serves older homeowners who want to access equity without selling their home.

Here’s what makes it different from traditional borrowing:

- You are not required to make monthly loan payments

- The loan balance increases over time instead of decreasing

- Repayment is delayed until a future event (sale, move, or passing)

Despite all this, ownership does not change. The home will remain in your name.

That’s an important point because many people hesitate simply due to a misunderstanding. They believe they’re having to sacrifice something.. In reality, they’re using their home equity differently.

For a local breakdown of these loans, review reverse mortgage loans in Rhode Island. It explains in-state eligibility and how payouts work.

For clear terms, especially if some words feel unfamiliar, the reverse mortgage glossary can help.

Why Reverse Mortgages Feel Different From Traditional Loans?

Numerous people try to understand a reverse mortgage by comparing it to a regular home loan. But this often creates confusion, not clarity. A reverse mortgage isn’t primarily about paying it back in the usual sense. They designed it around accessibility.

When you have a mortgage, everything is about whether you can pay it every month. With a reverse mortgage, the main thing is whether you can stay in your home for a long time. This small difference makes a change in how the reverse mortgage works.

This is why many Rhode Island homeowners see it less as “borrowing” and more as using a resource.

This is especially true in Providence or Warwick for those who have owned homes for decades. Taking on new debt isn’t the point—it’s unlocking something that has been sitting there unused.

How Reverse Mortgage Payments Work?

One of the most practical advantages of a reverse mortgage is how flexible the payment structure can be. It doesn’t force you into a single format.

Instead, you can choose based on your needs.

Lump Sum Option

Some homeowners prefer receiving a large amount upfront. People often use this to pay off an existing mortgage or eliminate other debts.

Monthly Income Option

This creates a steady stream of funds. It doesn’t count as income, but it works in a similar way to cover daily expenses.

Line of Credit Option

This is the most underappreciated feature. You don’t take the money right away. You access it when needed—and unused funds can actually grow over time.

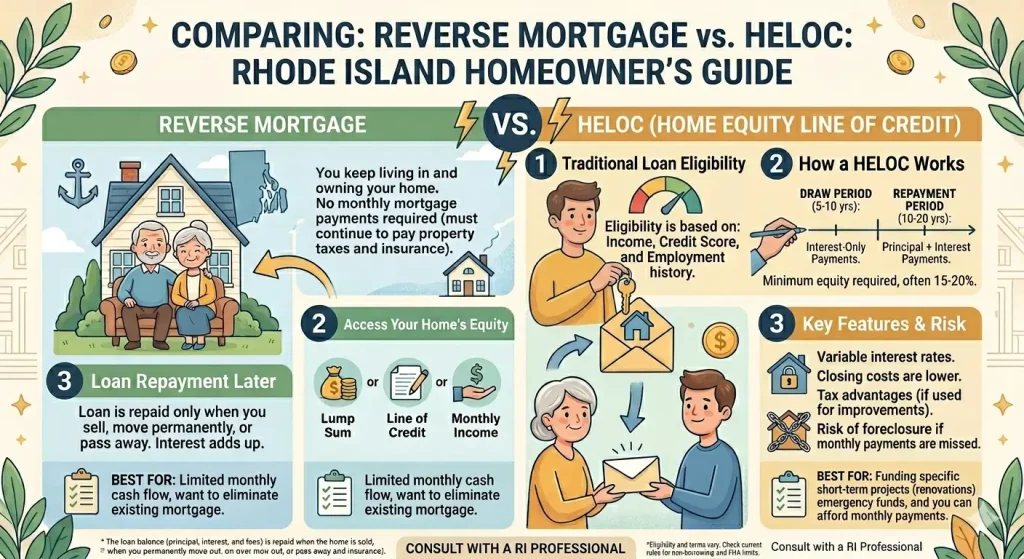

That built-in growth feature distinguishes it from a HELOC. With a HELOC, unused funds sit idle. With a reverse mortgage line of credit, available funds can increase.

To compare flexibility versus repayment obligations, the differences are clearer in a reverse mortgage vs HELOC.

Who Qualifies for a Reverse Mortgage?

Qualification is less about income and more about fundamentals.

You generally need to:

- Be at least 62 years old

- Live in the property as your primary residence

- Have sufficient equity in the home

- Stay current on taxes and insurance

There is also a financial assessment. This doesn’t function like a strict income check, but it ensures you can maintain the home.

For many retirees, this makes reverse mortgages a practical option. Regular loans usually depend on how much money you make. Reverse mortgages depend on the value of your home.

If you want to know all the details, you can look at the reverse mortgage qualifications. Each one is explained in detail.

How Much Can You Get?

This is usually the first practical question people ask.

The amount depends on:

- Your age

- Home value

- Interest rates

- Existing loan balance

Let us consider an actual case from Rhode Island.

The owner of a house worth $430,000 in Cranston can apply for a reverse mortgage starting at the age of 70. They can receive approximately 45% – 60% of the appraised value at this age.

That equals:

👉 $190,000 – $260,000 (without fees and pay-off).

These figures are not guaranteed values but provide valuable insight.

One thing people often don’t realize:

👉 The older you are, the more you can access.

That’s because the lender expects a shorter loan duration.

How Your Age Directly Affects Your Loan Amount?

Age plays a more important role in reverse mortgages than most people expect. Not just a requirement, it directly impacts how much money you can access.

The reason is really simple. Lenders figure out how long they think the loan will stay active. A 62-year-old borrower may get a loan because the loan is probably going to last a long time.

A homeowner who is in their 70s, on the other hand, may get a bigger loan amount because the expected duration is shorter.

This doesn’t mean waiting is always better. It simply means timing changes the outcome. For some homeowners, accessing a smaller amount earlier provides more value than waiting for a larger amount later.

Why Timing Matters More Than the Loan Type?

Most homeowners concentrate on which option is better, but many wonder when to use it. Timing plays a bigger part than people expect. Taking a reverse mortgage too early may limit long- term elasticity. Staying too long may mean missing years of fiscal comfort.

For illustration, a 62-year-old homeowner in Providence may qualify for a reverse mortgage. However, the available funds may be lower than for someone who is 70. On the other hand, delaying access to equity might force people to rely on savings they could have preserved.

This is why timing decisions are rarely just financial—they are strategic. Choosing this loan also means deciding the stage of life when it helps the most.

If you’re still comparing options before thinking about timing, review reverse mortgage vs. HELOC in a broader context.

Costs and Fees: What You’re Actually Paying For

Reverse mortgages are often criticized for being “expensive,” but that statement needs context. Yes, costs exist—but the structure differs from traditional loans.

Here’s what you’re paying for:

Origination Fee

Covers lender processing and underwriting.

Mortgage Insurance Premium (MIP)

This is what makes HECM loans federally protected. It ensures you never owe more than the home’s value.

Closing Costs

Includes appraisal, title services, and legal work.

Servicing Fees

Sometimes charged over time for loan management. Rather than paying these out of pocket, many borrowers roll them into the loan. For a breakdown review of reverse mortgage fees and closing costs.

How Interest Builds Over Time and Why It Matters?

One detail that frequently goes unnoticed is how interest behaves differently in a reverse mortgage compared to traditional loans. Since you make no yearly payments, the loan balance accrues interest over time. This means the total quantum owed slowly increases rather than reducing.

That doesn’t mean it’s a bad option, but it does change how you should approach it. Instead of focusing on whether you can afford it each month, the focus shifts to your home’s equity over time.

For homeowners who plan to stay in their home for years, this structure can make sense. But for those thinking about moving within a shorter timeframe, it may not align as well.

For a clear breakdown of how reverse mortgage interest works from a regulatory perspective:

👉 How reverse mortgage interest accumulates

Equity Position Over Time

Equity doesn’t disappear overnight with a reverse mortgage—it changes gradually. In the early years, the impact is often smaller than people expect. The loan balance grows slowly at first, especially if you are not using large amounts of the available funds.

Over a longer period, the effect becomes more noticeable. Interest accumulates, and the portion of the home you “own free and clear” reduces over time. However, this is only one side of the equation.

Rising property values can help offset some of the equity loss. As home prices continue to increase in Warwick and Cranston, they quietly affect this balance in ways that may not be obvious at first.

This is why you should focus on long-term property value trends instead of only considering short-term outcomes.

Real-Life Example: Patricia in Warwick

Patricia is 68 & has lived in Warwick for over 20 years. Her home is worth about $410,000. She has no remaining mortgage.

Her income is steady but limited—Social Security plus a small pension. Her concern isn’t immediate debt. It’s long-term stability.

Instead of selling or downsizing, she chooses a reverse mortgage. She sets it up as a line of credit.

Over time, she uses it to:

- Cover unexpected home repairs

- Supplement monthly expenses

- Handle rising healthcare costs

What changes for her is not just financial—it’s psychological. Now she feels financially secure, something many people tend to underestimate.

If you’re not certain this option fits you, checking is a reverse mortgage a good idea can give you a clearer perspective.

How Do You Repay a Reverse Mortgage?

Repayment doesn’t happen monthly. It happens later.

Typically, the loan is repaid when:

- The home is sold

- You move out permanently

- The property is inherited

At that point:

- The home is sold

- The loan balance is paid off

- Remaining equity goes to you or your heirs

If heirs want to keep the home, they can refinance or pay off the balance.

To understand this process better, see selling a home with a reverse mortgage.

Reverse Mortgage vs Other Options

| Feature | Reverse Mortgage | HELOC | Refinance |

| Monthly Payments | Not required | Required | Required |

| Income Dependency | Low | High | High |

| Best Use Case | Retirement cash flow | Short-term needs | Lower interest rate |

| Risk Type | Equity reduction | Payment increases | Ongoing obligation |

If you’re comparing broader strategies, reverse mortgage vs refinancing explains where each option fits.

For retirement-specific decisions, you can explore which is better for retirement.

Do You Keep Your Home?

Yes. You remain the homeowner. This is one of the most misunderstood aspects. The lender does not take ownership unless obligations are not met.

For clarity, read do you keep your home with a reverse mortgage.

The Trade-Off Most People Overlook

Every financial decision has a trade-off.

With a reverse mortgage:

👉 You gain cash flow

👉 You reduce future equity

With a HELOC:

👉 You preserve equity (if managed well)

👉 You take on payment responsibility

The right choice depends on what matters more:

- Stability now

- Or preservation later

Situations Where Other Options May Fit Better

When you think about a mortgage, it is a good choice but it is not the best choice for everyone. If you plan to move to another home in a few years, you may find that other options fit your plans better.

Some people have an income, and they are okay with making payments every month. For these people, they might like options better because they help keep the value of their house over time

Comparisons help here—not to find the “best” option, but the one that fits your needs.

If you’re considering alternatives, comparing reverse mortgages vs refinancing can show how each works over time.

Financial Flexibility Without Monthly Pressure

One of the most noticeable changes after taking a reverse mortgage is not just financial—it’s behavioral. Without a fixed monthly payment, financial decisions begin to feel less stressful.

Homeowners worry less about short-term costs when they don’t have fixed monthly payments. This doesn’t mean spending increases—it means pressure decreases.

Even without major financial changes, this can create a stronger sense of stability in retirement. The effect is small, but for many people, it becomes one of the most important parts of the whole retirement plan.

Why Some Homeowners Delay This Decision Too Long?

Hesitation often comes from uncertainty about timing, not lack of understanding.

Some homeowners wait until financial pressure becomes urgent. At that point, their options may be more limited. Some people avoid the decision altogether because they think they’re giving something up—even when that’s not true.

In reality, timing affects flexibility. Acting earlier doesn’t mean committing immediately—it means understanding your options before they become necessary.

Homeowners in Cranston often see better outcomes when they start exploring options early rather than rushing later.

Common Misconceptions

Many people stay away from mortgages because they have old or wrong information, about reverse mortgages.

Let’s clear a few:

“The bank owns your home.”

No—you retain ownership.

“You can be forced out.”

Only if basic obligations are not met.

“It’s only for people in financial trouble.”

Not true. Many use it as a strategic retirement tool.

Understanding these points changes how the product is viewed.

The Role of Reverse Mortgages in Retirement Planning

People are starting to see mortgages as a normal part of planning for retirement. Reverse mortgages are not something you do when you have no other choice. Some homeowners are using mortgages in a smart way. They are using the money from their home while keeping their investments safe.

This way of doing things can really help people make their retirement money last longer. It is especially helpful during years when the market is not doing well. Reverse mortgages also give people a safety net for expenses. They do not have to take money out of their retirement accounts when it’s not a good time to do so.

This is not a universal strategy, but it reflects a shift in how financial planners think about housing wealth. For many homeowners in Rhode Island, the home is their largest asset—and ignoring it entirely may not always be the most efficient approach.

If you’re still evaluating whether this fits your situation, reading is a reverse mortgage a good idea can help connect the strategy with real-life use cases.

How Reverse Mortgages Fit Into a Bigger Financial Plan?

A reverse mortgage is rarely used in isolation. It usually becomes part of a broader financial picture.

Some homeowners use it to delay drawing from retirement accounts. Others use it to create a backup source of funds for unexpected expenses. In both cases, the goal is not just access to money—it’s control over when and how that money is used.

This is where the conversation shifts from “Is this a good loan?” to “Does this support the way I want to manage my finances?”

That shift is important. Because once you start looking at it as part of a system rather than a standalone decision, it becomes much easier to evaluate.

FAQ (People Also Ask)

How does a reverse mortgage work in simple terms?

You receive money from your home equity, and repayment happens later when the home is sold.

Is a reverse mortgage a good idea?

It depends on your goals. It works well for reducing monthly financial pressure.

Can I lose my home?

Only if you fail to meet basic obligations like taxes and insurance.

What are the biggest costs?

Origination fees, insurance, and closing costs.

Can I exit early?

Yes, you can sell or refinance at any time.

How much can I borrow?

Typically 40%–60% of your home’s value, depending on age.

Does it affect Social Security?

No, it does not impact Social Security or Medicare.

What happens to my home after I pass away?

Heirs can sell or refinance the property.

The Quiet Advantage Most People Don’t Notice

There’s one advantage of reverse mortgages that rarely gets mentioned directly. It’s not the money. It’s the removal of pressure.

For homeowners who have spent years managing monthly obligations, the absence of a required payment changes how finances feel day to day. It creates space—mentally as much as financially.

That doesn’t show up in comparison charts. But it often becomes the deciding factor. For some, that shift matters more than interest rates or loan balances ever could.

Final Thoughts

A reverse mortgage is not about borrowing money in the traditional sense. It’s about reshaping how your home supports your life.

For some homeowners, it creates freedom. For others, it may not align with their goals. The key is understanding—not assuming.

Once you understand how it works, the decision becomes much clearer.

Talk to a Rhode Island Expert

If you need help thats just right for you talking to someone who knows your area can really help.

You can get in touch with RI reverse mortgage specialists or ask for a free consultation to look at what you can do, without being pushed.

Sometimes just talking to someone can make things clear. You don’t always need to do reading.