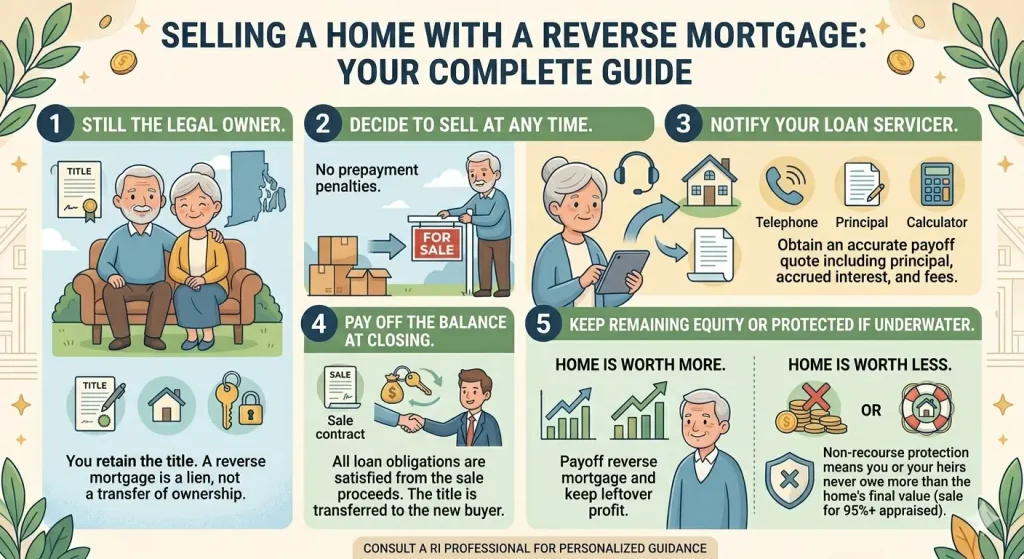

Yes — you can sell. That’s the simple answer most people are looking for. If you’re asking if you can sell a home with a reverse mortgage, you’re not stuck. You’re also not alone in wondering.

A lot of homeowners in Rhode Island reach this point after a few years. Maybe the house feels too big now. Maybe expenses have changed. Or maybe it’s just time for something different.

Whatever the reason, having a mortgage doesn’t stop you from selling your home. It just changes how you pay off the loan when you do sell.

In cities like Providence, Warwick, and Cranston, homes average about $430,000. Many homeowners still have money left after repaying the loan. That’s why this decision often comes down to timing and personal goals rather than limitations.

How Selling Actually Works

Selling a home with a mortgage looks a lot like a regular home sale. You put your home on the market, find a buyer, and close the deal. The difference happens behind the scenes.

When the sale is finalized, the seller uses the sale proceeds to pay off the reverse mortgage. The closing agent handles this part, so you don’t have to coordinate directly with the lender.

Once you pay off the loan, you keep whatever is left.

For most people, this is the moment where things “click.” The system is not complicated. It’s a structured way of settling the loan when the home changes hands.

If you have never checked how the balance grows over time, it can help to know how reverse mortgages work. This is especially true because interest adds up in a way compared to traditional loans.

Costs to Consider Before You Sell

Even though selling a home with a reverse mortgage follows a fairly simple process, there are still a few costs that come into play. Typical costs like agent commissions and closing fees are part of most home sales. With a reverse mortgage, you also need to pay off the loan.

That payoff usually includes the remaining balance along with interest that has built up over time. In some cases, the bill may also include service-related charges. None of this is hidden or unexpected. But it can affect how much money you take home after the sale.

Getting a rough estimate early helps you avoid surprises later. It also gives a more realistic idea of your final equity.

What If the Numbers Don’t Line Up?

This is usually the part that makes people pause. What happens if the home doesn’t sell for enough to cover the loan?

With a reverse mortgage, you’re protected. These loans are designed so that you never owe more than the home is worth at the time of sale. If the sale price comes in lower than the loan balance, the difference isn’t your responsibility.

That’s not something you see with most types of borrowing. It’s one reason reverse mortgages exist. They reduce risk for the homeowner, not increase it.

Some people only learn this detail years later, which often changes how they feel about the entire situation.

When It Becomes a Short Sale

Sometimes the sale price is lower than expected, and that’s where a reverse mortgage short sale comes into play.

It sounds more complicated than it usually is. In simple terms, the lender agrees to accept the market value of the home, even if it’s less than what’s owed.

There are a few extra steps involved, mainly lender approval. But it’s not like a traditional short sale,. Those can feel uncertain or take a long time.

In fact, because reverse mortgages already include protections, the process tends to be more structured.

Still, pricing matters here. Homes that are listed realistically from the beginning tend to move faster and avoid unnecessary delays.

Downsizing Isn’t Just About Money

A lot of people who own homes think selling is about money. Really, it’s often about how they want to live their lives.

Homes that used to be perfect can start to feel like a lot of work. They have much space, too much to clean, and too much to take care of. When people downsize, it’s not so much about losing something. About making life simpler.

You see this a lot in Rhode Island. People who have lived in their home for many years may look for a smaller home. It may be easier to care for. It may also be closer to family.

Selling a home with a reverse mortgage fits naturally into that transition. You close out the loan, keep whatever equity remains, and move into a setup that better matches your current life.

After a Spouse Passes Away

This is a tough situation, and people do not always talk about it. When one spouse dies, the other spouse can usually keep living in the home as long as they do what the loan says they have to do.

If the home is not used as the main place they live, the loan is due right away. At that point, selling is often the most practical option.

The process of selling a home does not change much. The timing of selling a home becomes very important. There is usually a set time to complete a home sale. Staying organized during this time helps you avoid stress.

It’s not just a financial decision, it’s an emotional one too, which is why transparency matters so much now.

What Heirs Should Expect?

When a home with a reverse mortgage is passed down, the responsibility doesn’t work the way people expect.

Heirs don’t inherit the loan in the traditional sense. Instead, they inherit the choice.

They can sell the home, refinance to keep it, or explore other ways to exit a reverse mortgage.

Most of the time, selling is the simplest route. The home is sold, the loan is repaid, and any remaining value becomes part of the estate.

What’s important to understand is that heirs aren’t personally responsible for covering any shortfall. That protection carries over, just like it does for the original homeowner.

A Quick Comparison That Helps

| Situation | Reverse Mortgage Sale | Regular Sale |

| Loan Payoff | Done at closing | Done at closing |

| Risk | Limited to home value | Borrower responsible |

| Process | Slightly more structured | Standard |

It’s not a completely different system—it just has a few extra guardrails.

Timing Makes a Bigger Difference Than People Think

One pattern shows up again and again. People wait. They wait until something forces the decision—financial pressure, health changes, or unexpected circumstances. At that point, the process can feel rushed.

People who own homes and think about selling their homes of time have more control over what happens to their homes. They get to decide when to sell their homes, how much money they want for their homes, and what kind of move is best for them.

It is not about rushing into things. It is about not waiting until people who own homes have no choice but to sell their homes.

How Timing Affects Your Selling Decision

Dealing with a home with a reverse mortgage isn’t only about whether you can sell it. It also comes down to timing. Some homeowners list their home when demand is high and prices stay strong. Others wait until market forces decide for them.

That difference can shape the entire outcome. When you plan, you usually have more room to decide your price, negotiate properly, and think through your next move. But if you wait until the loan becomes due or circumstances change suddenly, the process can feel rushed.

In Rhode Island’s market, even a small timing change can affect buyer interest. That is why when you sell matters as much as how you sell.

The Rhode Island Angle

Local market conditions are really important; they matter more than most people think. In places like Providence and Cranston, homes can sell fast if the price is right.

Even when the market is doing well, if you price your home too high, it can take longer to sell. You have to be careful with the price. It makes a difference.

And when a reverse mortgage is involved, timing can matter. If the loan has already become due, delays can add pressure.

That’s why working with someone familiar with both the market and reverse mortgages can make things smoother. Even a short conversation with an RI reverse mortgage broker can give you a clearer sense of direction.

When Selling Is Actually the Right Move

Selling isn’t always the answer—but sometimes it clearly is. If taking care of your home feels like too much, selling may help.

If your priorities have changed, selling may help. If you want a new living arrangement, selling may help. It’s less about the loan itself and more about where you are in life.

Understanding reverse mortgage eligibility can help you see the bigger picture. This is useful if you’re deciding to stay, sell, or change your plan.

A Helpful Outside Perspective

If you want a clear, no-pressure explanation of how these loans are structured, this reverse mortgage consumer guide is worth a look.

It explains things in plain language and can help confirm what you’re already learning.

Final Thoughts

If you’ve been asking if can you sell a home with a reverse mortgage, the answer is simpler than it seems.

You can sell. The loan gets paid off. And you move forward.

For many Rhode Island homeowners, that step becomes less about the mortgage. It becomes more about what comes next. It means less maintenance, less pressure, and a setup that fits their life now.

If you’re thinking about your next step, it might help to talk it through with someone who understands the process locally.

You can get expert guidance on your situation and figure out what makes sense—without feeling pushed in any direction.