Reverse mortgage terminology can feel confusing at first. Most people don’t even realize how important it is—until they’re sitting in front of paperwork they don’t fully understand.

Before signing anything, here are the 15 terms every RI homeowner must understand.

If you’re even slightly considering options like reverse mortgage loans in Rhode Island, taking a little time to understand these terms can save you from making a decision you regret later

This trend of taking reverse mortgages has been seen in areas similar to Providence, Warwick, and Cranston, where the price position of homes is estimated at $430K. Still, the reality of the situation is that the maturity of individuals is ignorant about the terminology involved.

And that’s where problems start.

Why These Terms Actually Matter More Than You Think?

Let’s be honest. Financial documents are not written for clarity. They’re written for compliance.

That means if you don’t actively try to define reverse mortgage terms for yourself, things can easily slip past you.

A small mistake, like not knowing how to pay back a mortgage or what extra costs are involved, can become a big problem later on.

On the other hand, when you understand what reverse mortgages are, everything gets better. You feel more in charge of your mortgage. You ask questions about your reverse mortgage. You do not feel like you have to rush into anything with your mortgage.

If you are still trying to figure out how does a reverse mortgage work, it is a good idea to learn about reverse mortgages and then look at this list of terms so you can see how the terms fit into the whole picture of reverse mortgages.

How Reverse Mortgage Language Can Affect Real Decisions?

There’s something people don’t talk about enough — the way financial language influences decisions.

When terms sound complicated, most homeowners do one of two things. They. Ignore these terms, or they think they will figure them out later. That’s risky.

Because in something like reverse mortgage terminology, small misunderstandings can lead to big differences in outcomes. For example, confusing “principal limit” with actual cash received can create unrealistic expectations.

This is why experienced advisors often suggest learning terminology before comparing loan options. It creates clarity early on.

If you’re exploring different structures or planning scenarios, reviewing broader loan options in Rhode Island can also help you see how reverse mortgages compare in real-world use

Quick Look: Core Terms You’ll Hear Again and Again

| Term | Simple Meaning | Why It Matters |

| HECM | Government-backed loan | Most common reverse mortgage |

| Principal Limit | Max borrowing amount | Determines your access to funds |

| MIP | Insurance fee | Protects your loan |

| Servicer | Loan manager | Your point of contact later |

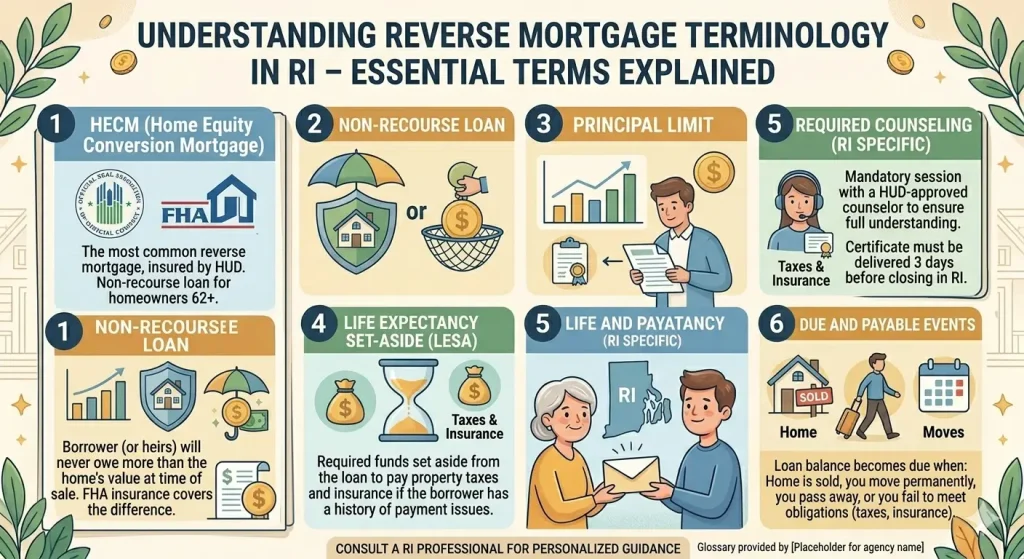

Reverse Mortgage Glossary (Real-World Definitions)

HECM (Home Equity Conversion Mortgage)

A HECM is the common type of reverse mortgage. The government backs it. Many homeowners in Rhode Island like this option. It seems secure to them. This is because it has rules to follow.

What makes it different is the level of structure and protection built into the loan. It’s designed to make sure borrowers are not exposed to unnecessary financial risk, even as the loan balance increases over time.

Because of this, most people exploring reverse mortgages end up considering HECM first before looking at any other alternatives.

Principal Limit

This is basically your borrowing ceiling.

It’s calculated based on your age, home value, and interest rates. Older homeowners usually qualify for more, which makes sense when you think about it.

Non-Recourse Loan

This is one of those terms that sounds technical but is actually very reassuring.

It means you or your family will never owe more than the home is worth. Even if the market drops, the lender cannot come after other assets.

MIP (Mortgage Insurance Premium)

MIP is required for federally insured reverse mortgages.

It might seem like an expense, but it has a reason. It safeguards both parties in the loan. Make sure you keep getting payments.

Origination Fee

This is what the lender charges to set up your loan.

It’s part of the overall cost structure, which is why reviewing reverse mortgage fees explained beforehand can help you avoid surprises.

Tenure Payment vs Term Payment

This is where things get more personal.

Tenure payments continue for as long as you live in the home. Term payments stop after a fixed period.

There’s no “better” option here—it depends on how you want your cash flow to work.

Line of Credit Growth Rate

This one surprises people.

If you don’t use your full credit line, the unused portion can actually grow over time. It’s not widely talked about, but it can be useful.

You can see how this works in practice through the CFPB reverse mortgage explanation where the growth feature is explained in simple terms.

Seasoning Requirement

Some lenders want to see how long you’ve owned your home before approving the loan.

It’s basically a stability check. Not always strict, but worth knowing.

HUD Counseling

Before things proceed, you have to do counseling with a HUD-approved agency.

In Rhode Island, agencies such as Money Management International and GreenPath Financial Wellness provide this service.

It is not a routine step. It is meant to protect you.

Servicer

After your loan is approved, the servicer takes over.

They handle your account, send statements, and answer questions. You’ll likely interact with them more than the original lender.

Due and Payable Clause

This defines when the loan must be repaid. Usually, it kicks in when you sell the house, move out for good, or die.

Non-Borrowing Spouse

If your spouse is not on the loan, things can get complicated. There are safeguards. They vary depending on the loan setup. This is something worth discussing early.

Maturity Event

This is simply the moment when the loan becomes due. It often overlaps with the due and payable clause but is used in more formal documentation.

Expected Interest Rate

This rate helps calculate your loan amount. It’s not always the rate you’ll pay, but it influences your principal limit.

Net Principal Limit

This is what you actually receive after fees. A lot of borrowers focus on the total amount, but this number is what really matters.

How Your Home Value in Rhode Island Impacts Your Loan?

Not all homes are treated equally in a reverse mortgage calculation.

In Rhode Island, where average home values are around $430K, your location plays a quiet but important role. A property in Providence may be evaluated differently compared to one in Warwick or Cranston due to market demand and appreciation trends.

This directly impacts your principal limit and the amount you can access.

👉 Home value is one of the biggest factors in reverse mortgage calculations

For further insight into the effects of valuations on borrowing, the FHFA house price index overview gives information about how local housing conditions affect loan approvals.

Having this knowledge will ensure that you manage your expectations accordingly.

Why Some Borrowers Use Reverse Mortgages as a Backup Strategy?

Not every homeowner takes a reverse mortgage for immediate cash. Some use it as a financial safety net.

They open a line of credit but don’t fully use it. Over time, that unused portion grows, creating a reserve they can rely on later.

This approach is often used by retirees who want flexibility without committing to withdrawals right away. It’s a quieter strategy, but a very intentional one.

If you’re still evaluating whether this approach fits your situation, understanding how does a reverse mortgage work in full context can help connect the dots

A Small But Important Rhode Island Insight

In Rhode Island, local factors can quietly impact your mortgage experience.

Property taxes, insurance costs, and even neighborhood trends in places like Cranston or Warwick can affect long-term results.

That is why looking at reverse mortgage eligibility requirements locally is more important than most people think.

When Most People Learn These Terms (And Why That’s a Problem)

Here’s something I’ve noticed. Most homeowners start learning these terms after they’ve already decided to move forward. At that point, they feel rushed.

They nod along. They assume they understand. But later, questions come up.

A better approach is simple: learn first, decide later. That way, when you speak with an RI reverse mortgage expert, the conversation actually feels like a discussion—not a sales pitch.

Common Mistakes That Are Easy to Avoid

Some mistakes don’t feel like mistakes at the time. People skip over details. They don’t ask follow-up questions. Or they assume all reverse mortgages are the same. They’re not.

Even understanding a few key reverse mortgage terms properly can prevent confusion down the line.

Final Thoughts

Understanding reverse mortgage terminology is not about memorizing definitions. It’s about making sure you’re not walking into something blindly.

Once the language makes sense, the decision becomes much clearer.

And if you still have questions, the best step is simple—get your questions answered — free consultation with someone who understands the Rhode Island market. Because clarity now can save you from confusion later.