For homeowners across Rhode Island, the house they bought years ago has become their biggest financial asset. Property values in places like Providence, Warwick, and Cranston have gone up, with the average home costing around $430,000. That kind of value changes how people think about retirement.

This is exactly where a Reverse Mortgage in RI starts to make sense. It’s not about taking on new debt or giving up your home. It is about using your home in a way that can help you without adding more bills to pay every month.

A lot of people do not understand what a reverse mortgage is. They are not sure about it. Once you get how it works, it is easier to think about whether it’s a good idea for you.

What Is a Reverse Mortgage?

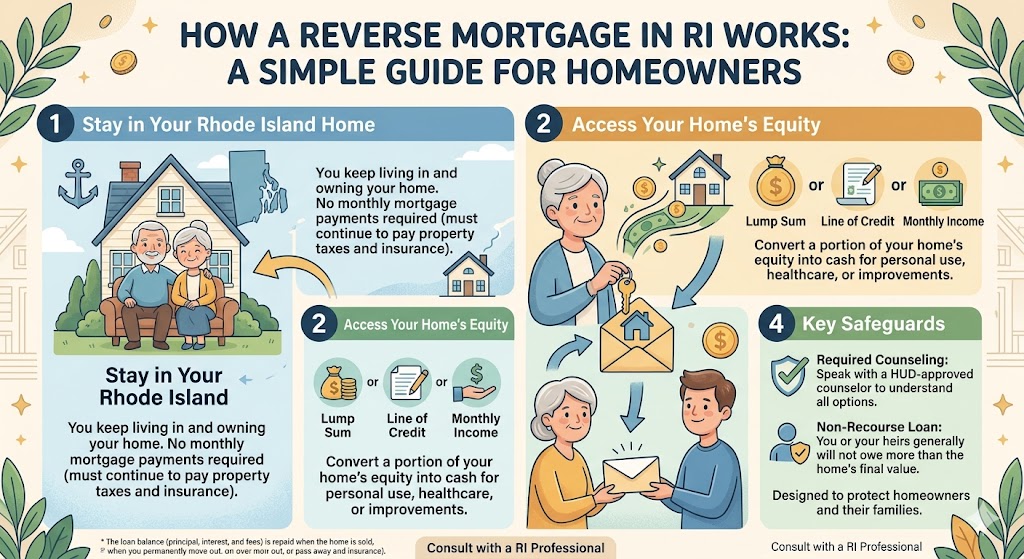

A reverse mortgage is a loan for homeowners who are 62 or older. It lets them turn some of their home equity into cash. The big difference between this and a regular mortgage is that the lender pays you, not the other way around.

You still get to own your home and live in it. You do not have to make mortgage payments. You pay back the loan later, usually when you sell your home, move out for good, or pass away.

This way of borrowing is different. It is not about whether you can afford to pay every month. It is about being able to stay in your home for a time. That is why a lot of retirees think of it as a tool to help them, not just a loan.

If you want to go deeper into how the structure works over time, you can read this detailed guide on how reverse mortgages work, which explains different scenarios in more detail.

HECM vs Proprietary Reverse Mortgage

Not all reverse mortgages are the same. It is a good idea to understand the differences now. The common type is the Home Equity Conversion Mortgage, also called HECM. The federal government backs this type of loan. It has built-in protections for borrowers. Many homeowners in Rhode Island choose this option.

On the other side, there are proprietary reverse mortgages. These are confidential loans offered by lenders and are frequently used for advanced- value homes where standard limits might not be enough. They can offer further elasticity, but they don’t always come with the same level of regulation as HECM loans.

For many people, particularly those just starting to explore options, HECM provides a more stable and predictable way.

Who Qualifies for Reverse Mortgage Loans in RI?

Qualifications for Reverse Mortgage Loans in RI differ from those for traditional lending. It’s not heavily concentrated on income or employment status, which is why it fits numerous retirees.

To qualify, you need to be 62 years old. You must live in the home as your residence. You need to have built up an amount of equity. You must stay current on property taxes and homeowners’ insurance.

There is a financial assessment. It checks if you can maintain the home. It does not judge your income like a loan would.

If you’re unsure, check if you qualify for a reverse mortgage. This step can clarify a lot of uncertainty.

How Much Can You Get in Rhode Island?

This is usually the first practical question people ask, and the answer depends on a mix of factors rather than a fixed number.

Your age is very important. Your home’s value, current interest rates, and any existing loan balance also matter. In Rhode Island, homes are worth around $430,000 on average. The numbers can add up.

For example, a homeowner in Cranston who is in their 70s might get between $190,000 and $260,000. This is not a guarantee. It gives you an idea.

One thing that surprises people is how much age matters with mortgages. The older you are, the more money you can usually get. That’s because the expected duration of the loan becomes shorter from the lender’s perspective.

How Payment Options Shape Your Financial Flexibility?

One of the reasons reverse mortgages are considered flexible is that they offer multiple payout options. Reverse mortgages let you choose what works best for you. You do not have to take one structure.

Some people like to get a lump sum. This is especially true if they want to pay off their existing mortgage. Others like to get payments. This creates an income. The line of credit option is often the best. It lets you get funds when you need them.

This is important when you compare options like a reverse mortgage vs HELOC comparison. The big difference is that you do not have to repay a mortgage right away. Unused funds do not earn interest over time.

How Payments Actually Work?

One of the reasons reverse mortgages feel flexible is that they don’t force you into one way of receiving money. Instead, you can choose what fits your situation.

Some people like a lump sum. They use it to pay off their mortgage or pay for something. Others, like payments. This gives them an income. Then there’s the line of credit option, which allows you to access funds only when needed.

This last option is often overlooked, but it can be powerful. Unlike traditional credit lines, unused funds can grow over time. That difference becomes clearer when you look at a reverse mortgage vs HELOC comparison, where HELOC funds typically remain static unless used.

Step-by-Step Application Process in RI

The process itself is more structured than complicated. It starts with an initial conversation where your situation is reviewed. From there, you complete the required counseling session.

Once that’s done, your home is appraised to determine its current value. The loan then moves through underwriting, where all details are verified before approval.

After approval, you move to closing. That’s when you finalize how you want to receive your funds.

The process is broken down into steps. It’s not too much to handle. Usually, things become clearer as you go through each stage, not all at once.

HUD Counseling Requirement in Rhode Island

People often forget about the HUD counseling session when they are thinking about getting a mortgage in Rhode Island. You have to talk to a HUD-approved counselor before you can even apply for a mortgage.

This counseling session is really important. It is not something you have to do. The counselor will explain how a reverse mortgage works and how much it will cost you over time. They will also tell you about options you might have. The counselor does not work for the lender, so they will give you advice that is just about your situation.

Most people in Rhode Island do these counseling sessions over the phone.. Sometimes you can do it in person, depending on where you live. You will talk about your money. Ask questions. After the session, you will have an idea if a reverse mortgage is right for you.

It might seem like a hassle. This counseling session is actually very helpful. It is one of the parts of the whole process, especially if you are just starting to think about getting a reverse mortgage. The HUD counseling session will help you understand mortgages in Rhode Island and make a good decision.

Pros and Cons You Should Actually Think About

Every financial decision comes with trade-offs, and a reverse mortgage is no different. The difference is in how those trade-offs show up over time.

In one sense, you gain flexibility because there are no monthly payments and you can stay in your home. That alone reduces financial pressure for many retirees. At the same time, the loan balance grows over time, which means your home equity decreases gradually.

The key isn’t whether this is “good” or “bad.” It’s whether that trade-off aligns with your priorities right now.

Pros and Cons of Reverse Mortgage

Every financial decision has pros and cons. It’s essential to look at both sides honestly.

| Pros | Cons |

| No monthly mortgage payments | Loan balance increases over time |

| Access to home equity | Reduces future equity |

| Stay in your home | Upfront costs may apply |

| Flexible payment options | Not ideal for short-term plans |

The goal isn’t to label it as good or bad—it’s to understand whether it aligns with your needs.

Reverse Mortgage vs Other Options

Many homeowners don’t consider mortgages on their own. They compare them with options before deciding what works best for them.

| Feature | Reverse Mortgage | HELOC | Refinance |

| Monthly Payments | Not required | Required | Required |

| Income Requirement | Low | High | High |

| Use Case | Retirement stability | Short-term needs | Rate reduction |

If you’re still comparing, looking at reverse mortgage vs refinancing your home can help clarify where each option fits long-term.

Why Regulation Matters in Reverse Mortgages?

Most people don’t really pay attention to this part, but reverse mortgages are regulated much more strictly than many other loan products. And that’s not by accident. The structure is intentionally designed to feel controlled rather than overly flexible.

The main reason is simple: these loans are built for older homeowners, where financial stability matters more than aggressive lending options. Because of that, reverse mortgages—especially HECM programs—are governed by federal rules that lenders must follow. They can’t randomly change terms, adjust conditions midway, or introduce unexpected requirements once the loan is in place.

Even the procedure itself is structured. From obligatory counseling to adopting limits and eligibility checks, everything is laid out step by step. At first regard, it may feel a bit restrictive compared to other fiscal products. But in reality, that structure is what protects homeowners from confusion later on. You already know the rules before you commit, which removes a lot of guesswork and uncertainty.

If you want to learn more about this framework, the Consumer Financial Protection Bureau’s reverse mortgage guide is helpful. Looking at an independent source like this is useful because it gives you a balanced view instead of relying only on a lender’s explanation.

A Small Detail Most Homeowners Realize Late

One thing that becomes clear after looking at enough real situations is that most homeowners don’t explore reverse mortgages until they actually feel financial pressure. It usually happens when monthly expenses start increasing, income doesn’t stretch as far as it used to, or savings begin to feel limited.

At that point, the decision often becomes reactive. Instead of comparing options calmly, people are trying to fix an immediate situation. That naturally reduces flexibility, because choices are made under pressure rather than planning.

On the other hand, homeowners who research reverse mortgages earlier, before they really need them, tend to have a different experience.

They have time to understand how it works, compare choices, and decide when it makes sense for their situation. There’s no rush, so opinions are generally more balanced and less stressful.

It may not seem like a difference at first but over time it can greatly affect financial comfort and how confidently someone manages their withdrawal planning.

Why Location Matters in Rhode Island?

Rhode Islands housing trends play a important role in this conversation. Cities like Providence, Warwick and Cranston have seen growth, in property values, which means many homeowners have a lot of equity without actively planning for it.

That creates an interesting situation. You might have significant wealth tied up in your home, but no easy way to use it without selling. A reverse mortgage simply creates access to that value while allowing you to stay where you are.

Common Misconceptions

A lot of hesitation comes from things people have heard over the years that aren’t entirely accurate.

Some believe the bank takes ownership of the home, which isn’t true. Others think they can be forced out unexpectedly, which only happens if basic responsibilities like taxes and insurance aren’t maintained.

There’s also a common idea that reverse mortgages are only for people in financial trouble. In reality, many homeowners use them as part of a broader retirement strategy.

Understanding these points often changes the entire perspective.

How It Fits Into a Bigger Financial Plan?

A reverse mortgage rarely stands alone. It usually becomes part of a larger financial picture.

Some homeowners use it to delay withdrawing from retirement accounts. Others treat it as a backup source for unexpected expenses. In both cases, the goal isn’t just access to money—it’s control over when and how that money is used.

If you want to better understand the language used in these decisions, reviewing reverse mortgage terms explained can make things easier to follow.

FAQs

How does a reverse mortgage work in RI?

It allows homeowners to access equity while staying in their home, with repayment happening later.

How much can I borrow?

Typically, between 40% and 60% of your home’s value, depending on age and conditions.

Can I lose my home?

Only if you fail to meet obligations like taxes and insurance.

Is it better than a HELOC?

It depends on your situation, which is why a reverse mortgage vs HELOC comparison is helpful.

Final Thoughts

A Reverse Mortgage in RI isn’t about rushing into a decision. It’s about understanding what’s available to you and deciding if it fits your life.

For some, it creates flexibility and peace of mind. For others, it may not be the right fit. The important thing is making that decision based on clarity, not assumptions.