Buying a home is one of the biggest steps in life. For many veterans and service members in Rhode Island, this dream feels out of reach. Rising property prices, expensive rent, and the thought of saving a huge down payment often make homeownership seem impossible.

However, VA loans provide a solution. They are designed to help veterans, active-duty members, and even certain surviving spouses. So, why are VA loans unique? Unlike FHA or conventional mortgages, VA loans allow you to buy a house with a VA home loan without a down payment.

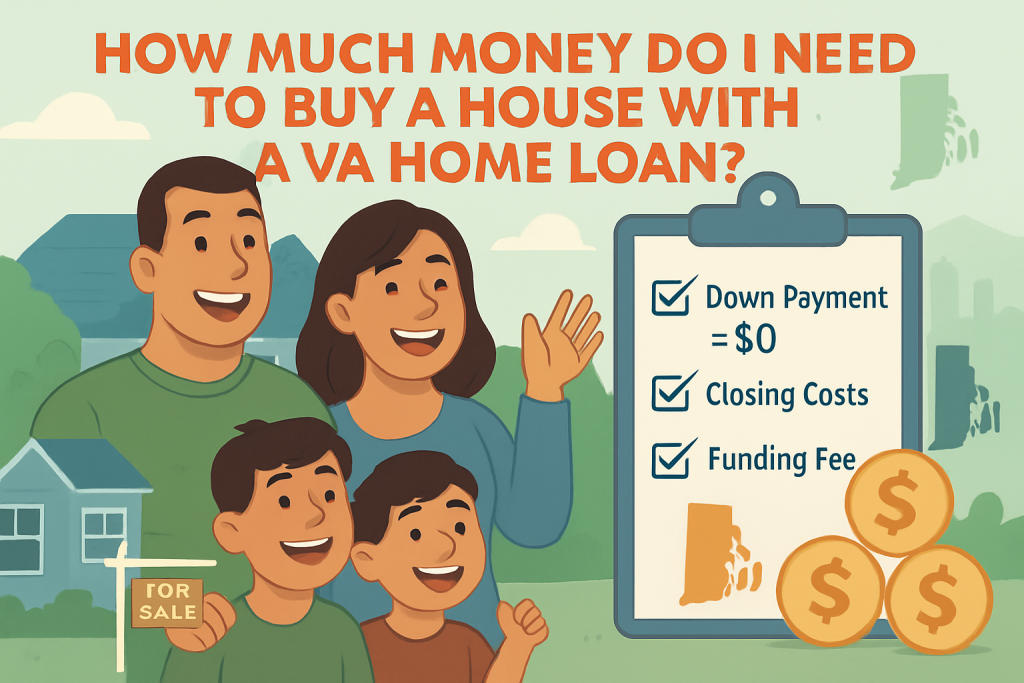

It is a huge relief for many families. Imagine skipping the need to save $20,000, $40,000, or even $80,000 before you can move forward. That’s the power of this benefit. You don’t need to bring a mountain of cash, but you cannot walk in with absolutely nothing either. That’s why understanding how much money you need to buy a house with a VA home loan is so important.

Do VA Loans Really Mean $0 Down?

The biggest advantage of a VA loan is often summed up in three words: no down payment. But what does that really mean in practice? Let’s look closer.

-

Comparing VA Loans to FHA Loans

With FHA loans, you must put at least 3.5% down. That may not sound like much at first. However, on a $400,000 home, it adds up to $14,000 upfront. For many first-time buyers, especially in Rhode Island, that number can be overwhelming. Saving that much can take years, and during that time, home prices may continue to rise.

-

Conventional Loans vs VA Loans

Now, let’s compare with conventional loans. In this case, brokers usually expect anywhere from 5% to 20% down on the same $400,000 property, which equals $20,000 to $80,000 upfront. Clearly, this amount is often out of reach for many military families. However, when you buy a house with a VA home loan, that entire down payment disappears. In fact, you can finance 100% of the purchase price. That’s right—zero dollars upfront for the down payment. Ultimately, it is not just a benefit; rather, it is truly life-changing.

-

The Truth Behind “$0 Down”

However, it is important to clear up a common misunderstanding. “$0 down” does not mean “$0 cost.” You will still need to cover other expenses. These include the VA funding fee, closing costs, and standard homeownership expenses like inspections or insurance. So, while you don’t need a massive upfront sum, you still must prepare wisely.

Upfront Costs You Still Need to Budget For

Even without a down payment, there are a few upfront expenses. Planning for these helps avoid surprises.

-

VA Funding Fee

The VA funding fee is a one-time payment. It helps keep the VA program running for future service members. The amount depends on whether this is your first VA loan or a subsequent one.

- First-time use: 2.3% of the loan amount

- Subsequent use: 3.6% of the loan amount

If you buy a $400,000 house with a VA home loan, your funding fee could be $9,200 (first-time use). The good news is that you can roll this into the loan instead of paying it up front. Even better, veterans with a service-connected disability are exempt.

-

Closing Costs

Closing costs are part of every mortgage, whether VA or not. They typically include appraisal fees, title insurance, credit report fees, origination charges, and more. In Rhode Island, closing costs usually range from 2% to 5% of the purchase price. For example, that means $8,000 to $20,000 on a $400,000 home.

But don’t worry, because VA rules limit how much you must pay. In addition, the seller can cover some fees. Furthermore, others can be offset with broker credits. Therefore, by working with RI Mortgage Brokers, you can negotiate these costs more effectively.

-

Home Inspection and Appraisal

The VA requires an appraisal to ensure the property is worth the price and meets minimum standards. You may also choose to pay for a private home inspection. These are smaller costs—usually a few hundred dollars—but they matter.

Ongoing Monthly Costs After Buying

After closing, you’ll face monthly expenses. Planning for them is essential.

-

Mortgage Payment (Principal & Interest)

Your monthly mortgage is based on loan size and interest rate. VA loans typically have lower rates, saving you money over time.

-

Property Taxes in Rhode Island

Property taxes vary by city. For example:

- Providence: about $18 per $1,000 value

- Warwick: about $14 per $1,000 value

- Cranston: about $17 per $1,000 value

That means taxes can add several hundred dollars each month.

-

Homeowners Insurance

It protects your property and belongings. In Rhode Island, average annual premiums range from $1,200–$1,800, depending on location and coverage.

-

HOA Fees

If you buy in a condo or planned community, you may owe monthly homeowners’ association fees. These vary widely.

Comparing VA Loan Costs to FHA and Conventional Loans

Here’s a quick look at how the three main loan types compare.

| Features | VA Loan | FHA Loan | Conventional Loan |

| Down Payment | 0% | 3.5% | 5-20% |

| PMI / MIP | None | Required | Required if under 20% down |

| Funding Fee | Yes (waived if disabled) | None | None |

| Credit Requirements | Flexible | More Flexible | Stricker |

| Best For | Veterans, Service Members | First-Time Buyers | Strong Credit Buyers |

This makes it clear. If you want to buy a house with a VA home loan, you save money upfront and every month. No PMI alone can save hundreds per month.

Example Scenario: Buying a $400,000 Home in Rhode Island with a VA Loan

Let’s walk through an example.

- Home Price: $400,000

- Down Payment: $0

- Funding Fee: $9,200 (if not exempt, can be rolled in)

- Closing Costs: $8,000–$12,000 (can be reduced with seller credits)

So, the total upfront cash needed could be as low as $8,000 if seller concessions are negotiated. Compare that with $20,000–$80,000 for conventional loans.

How to Reduce Out-of-Pocket Costs with a VA Loan

Even though costs with a VA loan are already much lower than other mortgage options, the good news is that you can actually reduce them even further. With the right planning, careful negotiation, and smart use of available benefits, you could save thousands of dollars. Step by step, let’s look at the main strategies.

-

Seller-Paid Closing Costs

To begin with, VA rules allow sellers to pay part of your closing costs. This is a major advantage because closing costs often add up to thousands of dollars. However, these savings do not happen automatically. Instead, they require negotiation.

Therefore, you need a skilled real estate agent and a knowledgeable VA loan specialist on your side. With their help, you can request the seller to cover a portion of your expenses. As a result, you walk into your new house with a VA home loan while keeping more cash in your pocket.

-

Broker Credits

In addition to seller help, you can also benefit from what brokers call “broker credits.” In this option, the broker agrees to pay part of your upfront costs. In return, you accept a slightly higher interest rate. At first glance, this may look like a trade-off. However, it can be very helpful for buyers who need to lower immediate expenses.

For instance, imagine you plan to refinance within a few years. Or maybe you intend to sell your home soon. In those cases, the small increase in your rate may not matter much. Yet, the short-term savings will make a big difference. Therefore, broker credits are worth considering when buying a house with a VA home loan in Rhode Island.

-

Funding Fee Exemption

Another powerful way to save money is through the VA funding fee exemption. Normally, this fee can add thousands of dollars to your loan. For many buyers, it becomes one of the largest upfront charges. However, if you are a disabled veteran who receives VA compensation, you are fully exempt.

As a result, you skip this cost completely. That means more savings and less stress during the buying process. This exemption alone can make a house with a VA home loan far more affordable, especially for veterans on a fixed income. So, always check your eligibility before assuming you must pay the funding fee.

-

Local Rhode Island Programs

Finally, let’s not overlook local programs in Rhode Island. Many communities here provide extra support to veterans and active-duty service members. For example, some towns offer property tax exemptions. Others provide housing grants or down payment assistance.

When you combine these local benefits with your VA loan, the savings really add up. In fact, these programs can reduce monthly costs, lower upfront expenses, and improve long-term stability

When you work with RI Mortgage Brokers, you do not have to figure all of this out alone. Their team understands VA loan rules, local programs, and broker credit options. Consequently, they can guide you step by step so that you minimize costs and make the most of your VA loan benefits.

Why Pre-Approval Matters for VA Loan Buyers

When planning to buy a house with a VA home loan, one of the smartest steps is getting pre-approved. But why does this matter so much?

- First, pre-approval shows you how much home you can actually afford. Instead of guessing, you see real numbers based on your income, credit, and debts. As a result, you can shop with confidence.

- Second, sellers take you more seriously. In a competitive market like Rhode Island, a pre-approval letter makes your offer stronger. Therefore, it can even help you win over other buyers.

- Third, pre-approval helps you avoid surprises later. Because brokers review your finances upfront, you know what to expect when it’s time to close.

Conclusion: Planning Your VA Home Purchase in Rhode Island

So, how much money do you really need to buy a house with a VA home loan? Well, the truth is simple. You actually need far less than most people expect.

First of all, you do not need a down payment. That means you can finance 100% of the home’s value. In addition, you do not pay PMI, which is a cost many FHA and Conventional buyers cannot avoid. Furthermore, your upfront costs are mainly closing costs and, in some cases, a funding fee.

Moreover, monthly payments often remain manageable. It happens because VA loans usually come with lower interest rates. On top of that, property tax savings in Rhode Island can also reduce long-term expenses.

Therefore, for veterans and service members in Rhode Island, this path is by far the most affordable way to become a homeowner. With the expert guidance of Mortgage Brokers, you can prepare, qualify, and move forward with confidence.

FAQs

1. Can I really buy a house with a VA home loan and no down payment?

Yes, absolutely. With VA loans, you can finance 100% of the purchase price. It means no down payment is required at all. However, it is important to remember that you still need to budget for closing costs.

2. What is the VA funding fee, and do I always have to pay it?

The VA funding fee is a one-time charge that helps sustain the VA loan program for future borrowers. Typically, it is 2.3% for first-time users and 3.6% for those using it again. Nevertheless, disabled veterans are completely exempt.

3. Are VA loans really cheaper than FHA or Conventional mortgages?

Yes, in most cases they are. Here’s why. VA loans require no down payment, unlike FHA and Conventional options. Plus, you avoid PMI altogether, which cuts hundreds from monthly bills. On top of that, VA loans usually carry lower interest rates.